How to assess a company that files no profit figure: a worked example

A real UK company that files no profit and loss account, and a real CIQ Score of 78. A worked example of making a sound credit decision from the balance sheet alone, when there is no profit figure to fall back on.

A company you are about to extend terms to is an established engineering consultancy, incorporated in the late 1990s, so more than twenty-five years of trading behind it. You go to check the accounts before you say yes, and you hit the wall this article is about: there is no profit and loss account. No revenue figure, no profit figure, nothing about how the business actually performed last year. Under the small companies exemption, it has filed only a balance sheet, which is entirely legal and, for a firm this size, completely normal. The question is whether you can still make a sound credit decision on what remains, and the answer is that you can.

This is a worked example of doing exactly that. A real UK company with real filed accounts, anonymised because the point is the method, not the company.

The score, before the detail

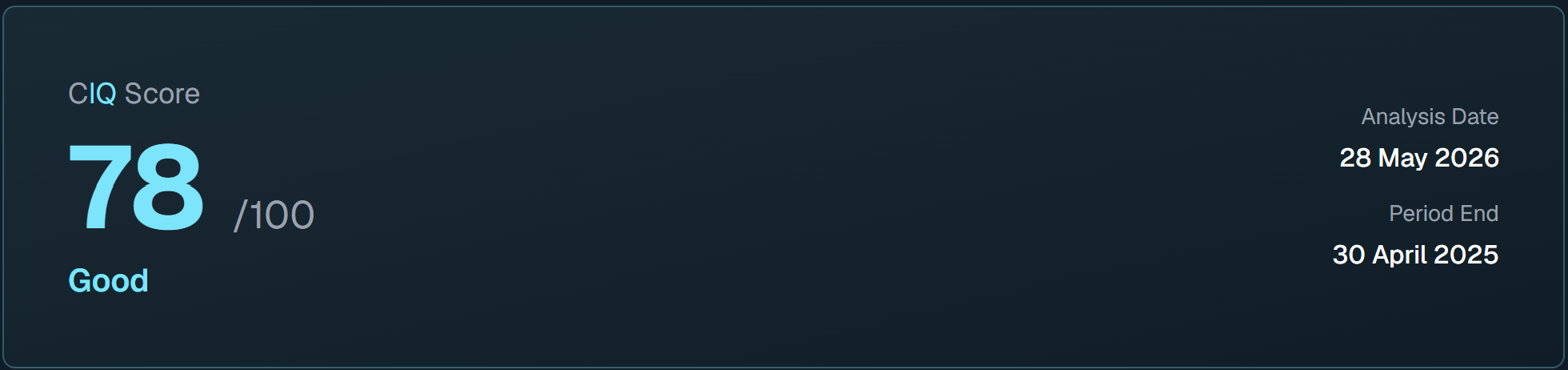

CompanyIQ scored this company 78 out of 100, which is a Good rating, the band you can extend terms to with normal monitoring. That is the conclusion. What makes this company worth walking through is how the analysis reached it without ever seeing a profit figure, because the route it took is the route you would take yourself once you know where to look.

What you cannot see

There is no turnover line, no profit before tax, no margin, and none of the figures most people treat as the heart of a credit check. For most of the UK companies you deal with, this is the situation, because the majority file under the same exemption.

The figures that actually tell you whether you will be paid were never in the profit and loss account to begin with. They are in the balance sheet, which this company, like every company, however small, is required to file. The balance sheet answers two questions, and between them, they carry most of a credit decision.

The first question: do they owe more than they own?

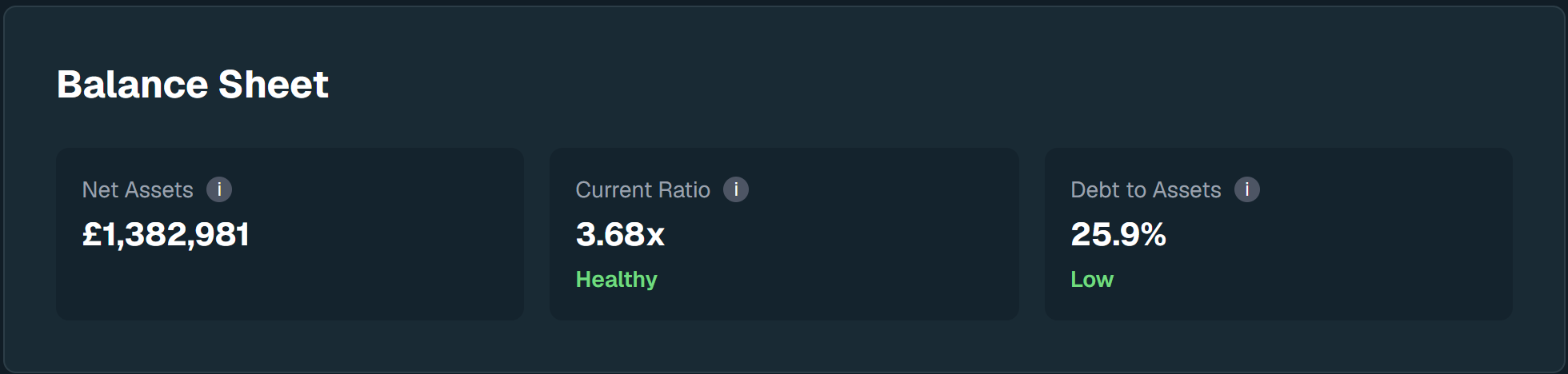

Net assets are everything the company holds set against everything it owes, and here they stand at £1,382,981, comfortably positive and slightly up on the prior year. The business owns well over a million pounds more than it owes, which is the first and most important reassurance you can take from a set of filleted accounts. There is no minus sign here, and a minus sign is the thing you are checking for. The company is solidly solvent.

The second question: can they cover what's due?

The current ratio measures whether the company can meet what falls due over the coming year, and at 3.68 it is marked Healthy, well above the level most credit policies look for. In plain terms, the company holds more than three and a half times the liquid resources it needs to cover its short-term obligations, with cash of £474,280 behind that. This is not a business that will struggle to pay its bills in the near term, and you can see that without a single line of the profit and loss account.

The third figure, debt to assets at 25.9% and rated Low, rounds out the picture. It does include a modest secured bank loan of around £160,000 running beyond a year, so this is not a wholly debt-free balance sheet, but a quarter of assets financed by liabilities is conservative by any measure, and it leaves significant headroom. A company carrying light, well-covered borrowing is not a concern; it is normal, sensible financing.

The warning signs: all clear

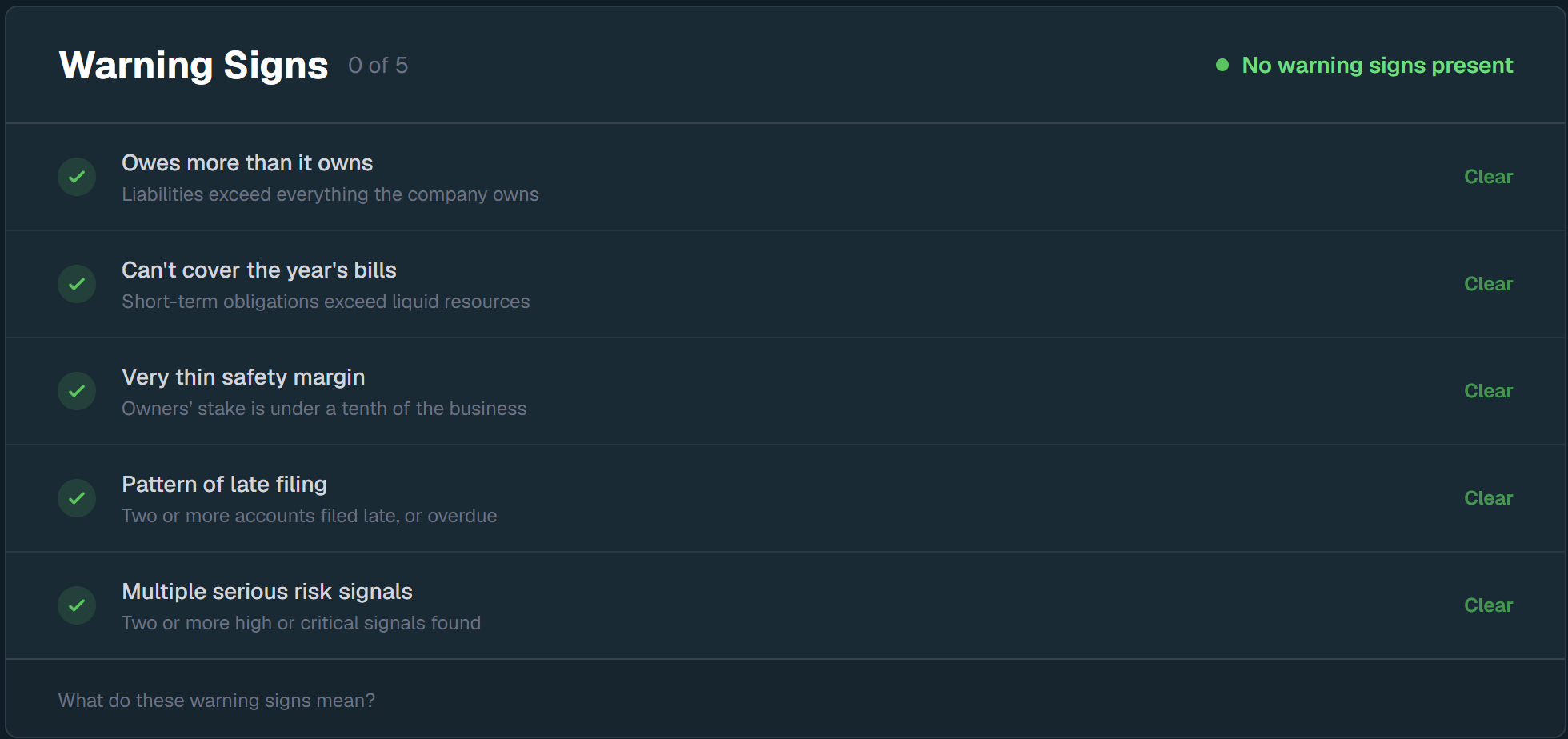

The five plain-English checks the analysis runs against every report read off the same balance sheet, and for this company, every one comes back clear.

It does not owe more than it owns, it can comfortably cover the year's bills, its safety margin is far from thin, there is no pattern of late filing, and there are no serious risk signals stacked up. None of the five things that, in a study of a hundred real company failures, tended to appear together in the businesses heading for trouble. The card reads zero of five, and on a company with no profit figure filed, that clean sweep is drawn entirely from the balance sheet and the filing record.

What you lose without the profit figure, and how to get some of it back

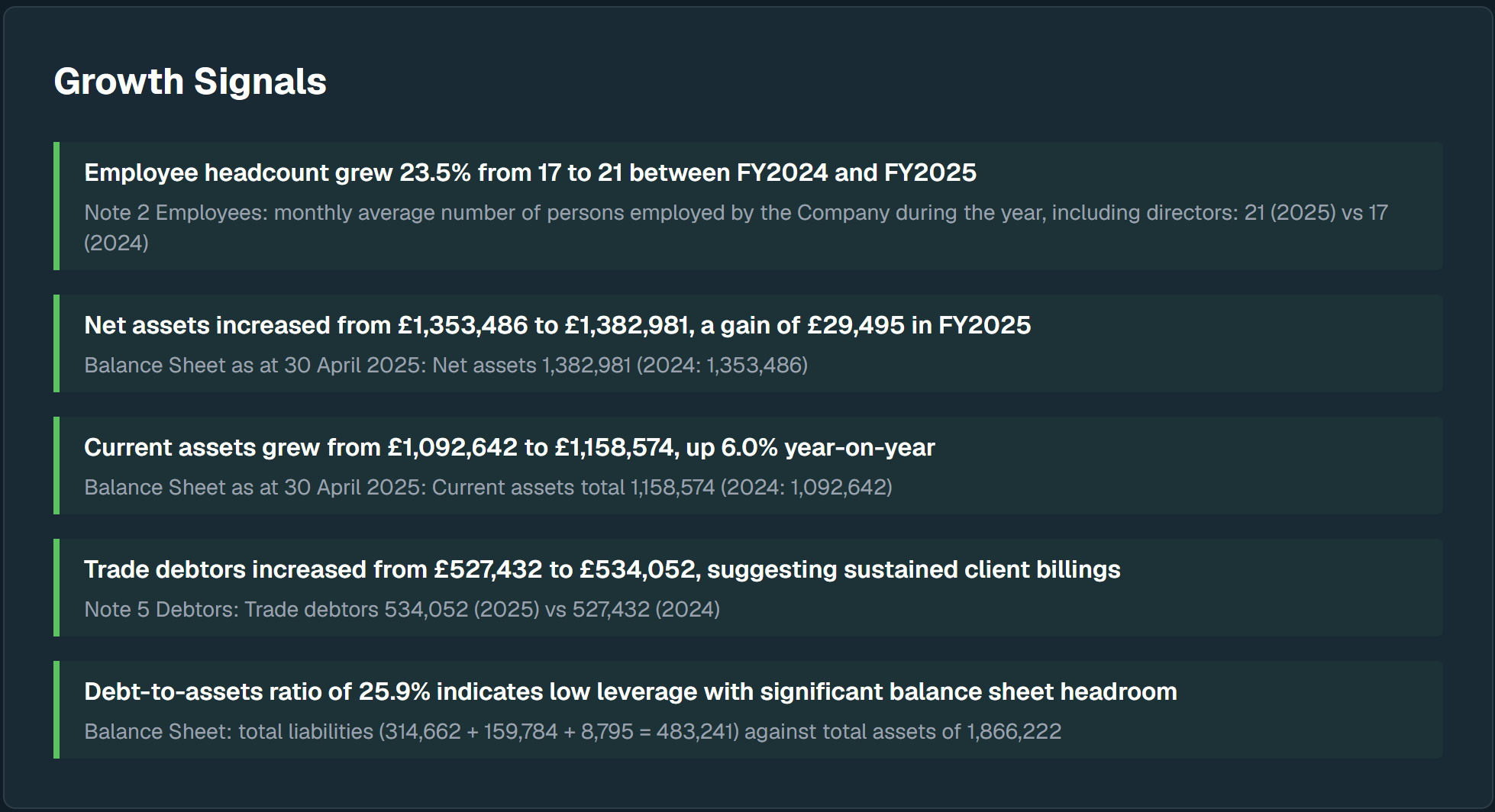

It would be dishonest to pretend nothing is lost. A profit and loss account would tell you the direction of travel, whether the company is growing or shrinking, and that is absent here. But you are not as blind to it as the missing statement suggests, because comparing two years of balance sheets recovers much of the trajectory.

On that comparison, this company is plainly moving in the right direction. Net assets are up year on year, current assets have grown by 6%, trade debtors are slightly higher, suggesting sustained client billing, and headcount has risen from seventeen to twenty-one, a 23.5% increase that points to a business taking on more work rather than retrenching. No single one of these is a profit figure, but together they sketch the shape of a firm that is expanding, and that shape is visible to anyone willing to read two filings instead of one.

The board

The last piece of a credit decision is who is behind the company, and here, the analysis found the most reassuring profile there is. The leadership is founder-led, with an average tenure of more than sixteen years, excellent stability, zero red flags, no disqualifications, and no trail of dissolved companies. Stable, long-serving leadership is one of the predictors of a company that pays its way, and this company has it in full.

The decision

So, back to the question you started with. An established consultancy wants terms, and its accounts carry no profit figure at all. The instinct says you cannot properly assess it, but the balance sheet says otherwise: a solidly solvent business, with more than three times the liquidity it needs, conservative borrowing, a clean filing record, no warning signs, a board that has run the firm steadily for over a decade and a half, and a two-year trend pointing upward.

Extend the terms. The missing profit figure was never the thing that mattered.

The profit and loss account answers how last year went. The balance sheet answers whether the business can survive next year, and when you are deciding whether to extend credit, that is the question that counts. The number people reach for first is the one that is missing, and the numbers that tell you whether you will be paid are the ones that are always there.

This entire analysis came from one search on CompanyIQ, and most analyses complete in 60 to 90 seconds. If you want to understand what a balance sheet reveals when there is no profit figure to fall back on, you can read the fuller explanation on the How It Works page, or run your first company at company-iq.co.uk.

Try CompanyIQ

Run a full analysis on UK companies in minutes. From £0.50 per report.