How to assess a company that doesn't file a profit and loss account

Most small UK companies file no profit and loss account. Here is what to read on the balance sheet instead.

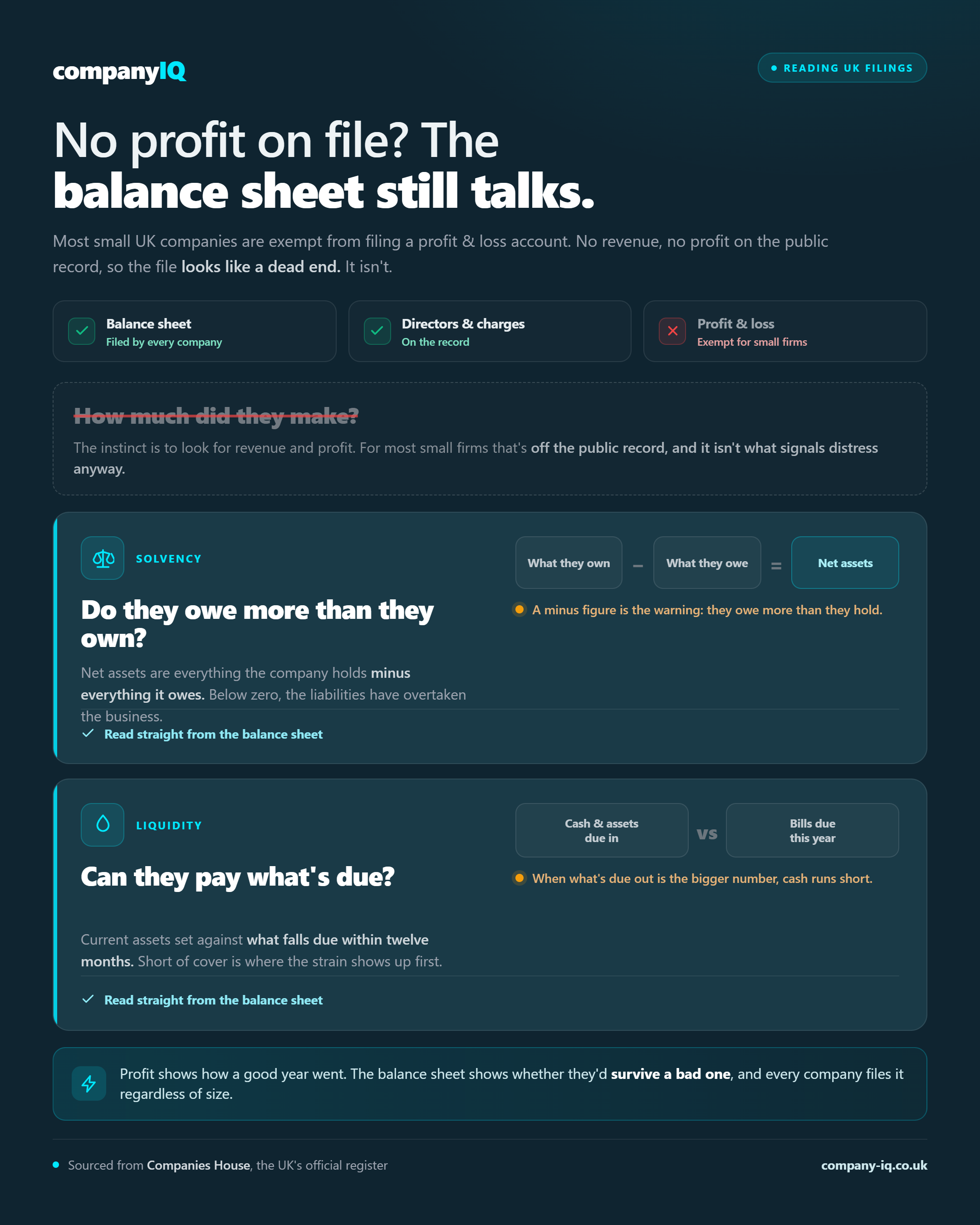

For most UK companies you might deal with, you cannot see what they earned or whether they made a profit at all. Small companies and micro-entities are allowed to file abbreviated accounts that leave the profit and loss account out entirely, and the majority of them take that option. When you go looking for a turnover line or a profit figure to judge whether a company is worth trading with, it simply isn't there, and the file can look like a dead end.

It isn't one, and this post is about why, and about what you should read instead.

Why the profit figure is missing

The absence is rarely anything sinister. Under the Companies Act, smaller businesses can file what are formally called filleted accounts, filing the balance sheet they are required to lodge while omitting the profit and loss account that larger companies must publish. The thresholds are generous, so the great majority of active UK companies qualify, and most of them use the exemption simply because there is no reason not to. A missing profit figure tells you almost nothing about the health of the business. It tells you only that the company is small enough to keep that figure private, which describes most of the companies you will ever assess.

So the instinct to hunt for revenue and profit, and to treat their absence as a warning, leads you nowhere useful. The reassuring part is that the absence does not actually blind you, because the figures that can predict trouble were never in the profit and loss account to begin with. They are on the balance sheet, and every company, however small, files one.

The first question: do they owe more than they own?

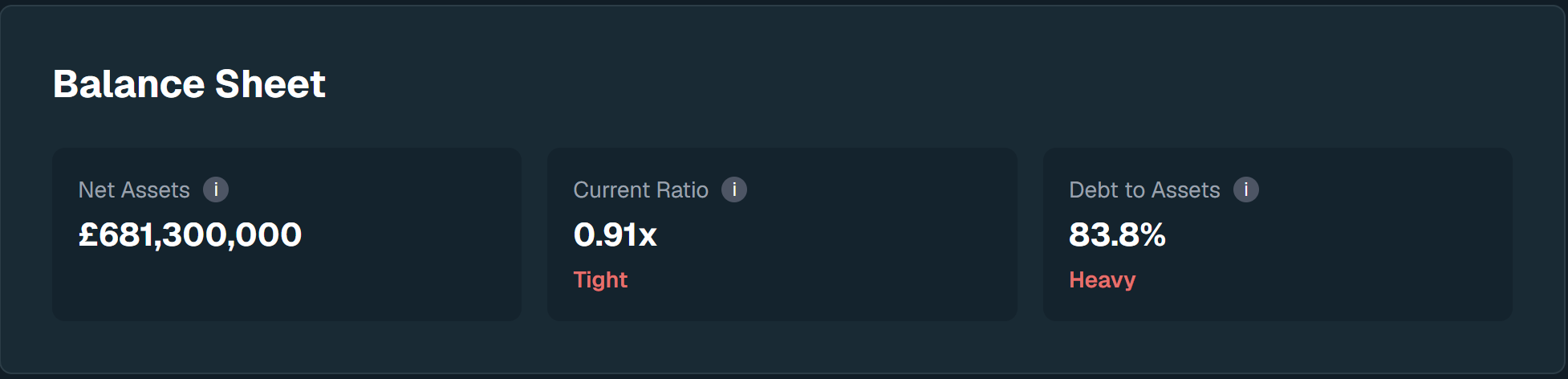

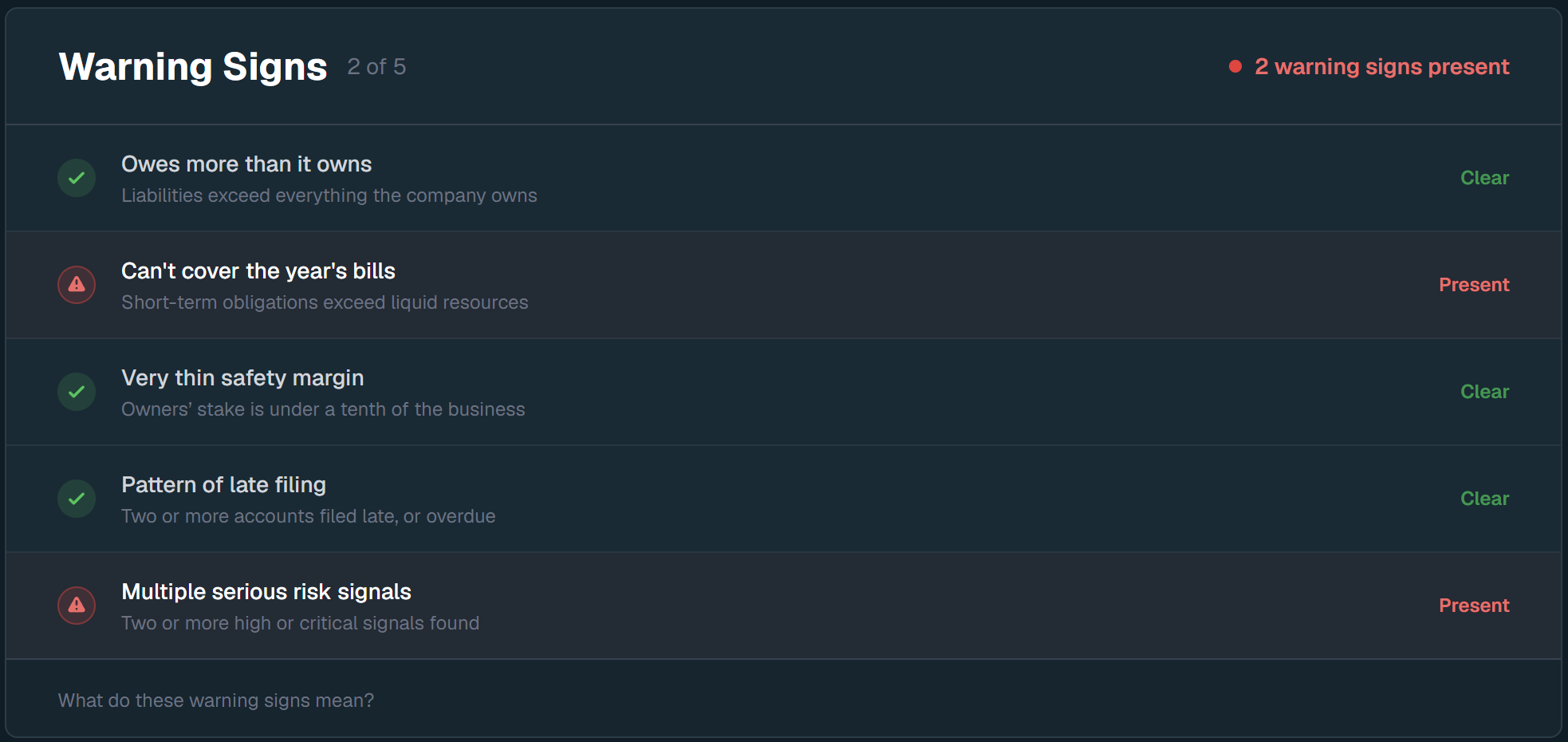

The balance sheet sets out everything a company holds against everything it owes, and the difference between the two is its net assets. When that figure is positive, the business owns more than it owes and has a cushion to absorb a bad year. When it is negative, the liabilities have overtaken the company, and it owes more than it could pay back, even if it sold everything it had. In the language we use on every report, this is the check for whether a company owes more than it owns, and a negative net asset position is one of the clearest signals of distress you can read from a filing.

You do not need to calculate anything. The net assets figure sits on the face of the balance sheet, and a minus sign in front of it is a warning. It is the single most useful number in a set of filleted accounts, and it is always there.

The second question: can they cover what's due?

The second question the balance sheet answers is whether the company can meet its obligations over the coming year. Current assets, the cash a business holds and the money owed to it that it expects to collect soon, are set against the liabilities that fall due within twelve months. When what is coming in comfortably exceeds what must go out, the company has room to breathe. When the bills due this year are the larger number, cash is tight, and tight cash is very often where the strain shows up first, well before a company formally fails. This is the check for whether a company can cover the year’s bills, and like net assets, it reads straight off the filed balance sheet without any need for the missing profit figure.

A third reading, how thin the equity cushion has become relative to the company’s total liabilities, rounds out the picture, but the two questions above carry most of the weight. Between them, they tell you whether a company is solvent and whether it can pay its way, which are the two things that actually determine whether you will be paid.

What you lose, and how to recover some of it

None of this is to pretend that the profit and loss account is worthless. A company can be sound on its balance sheet and still be sliding, losing money each year and eating into reserves that once looked healthy, and that trajectory is exactly what a profit and loss account would show you. When it isn’t filed, you lose that sense of direction.

You can recover some of it by comparing two years of balance sheets rather than reading one in isolation. If net assets are shrinking year on year, if cash is thinner than it was, if the company owed less twelve months ago than it does now, the direction of travel is visible even without a single profit figure. One balance sheet is a snapshot; two is the beginning of a trend, and the trend is often the more telling of the two.

The figure people reach for first is rarely the one that matters

The deeper point is that profit answers a different question from the one a supplier or a lender is really asking. Profit tells you how last year went. The balance sheet tells you whether the business can survive next year, and when you are qualifying a lead or deciding whether to extend credit, survival is the question that counts. The number people instinctively reach for first is the one that is missing, and the numbers that genuinely tell you whether you will be paid are the ones that are always there, sitting in plain sight, waiting to be read the right way.

That this holds is not a matter of opinion. When we scored 100 UK companies that had gone into insolvency, 91 of them were abbreviated filers with no profit figure on record, and they were flagged as troubled at almost the same rate as the companies that had published everything. The missing profit line hid nothing that mattered. You can read the full study here.

CompanyIQ reads these checks from the filed balance sheet automatically, on every company, including the ones that file no profit figure at all, and shows them as a set of plain-English warning signs alongside the score. You can see exactly what it looks for on the How It Works page.

Sign up for a free UK company analysis

CompanyIQ reads the filed accounts and returns a scored report in 60 to 90 seconds.

Run a company checkFirst analysis free, no card required. After that, £15 for a one-off or from £0.50 each on a plan.